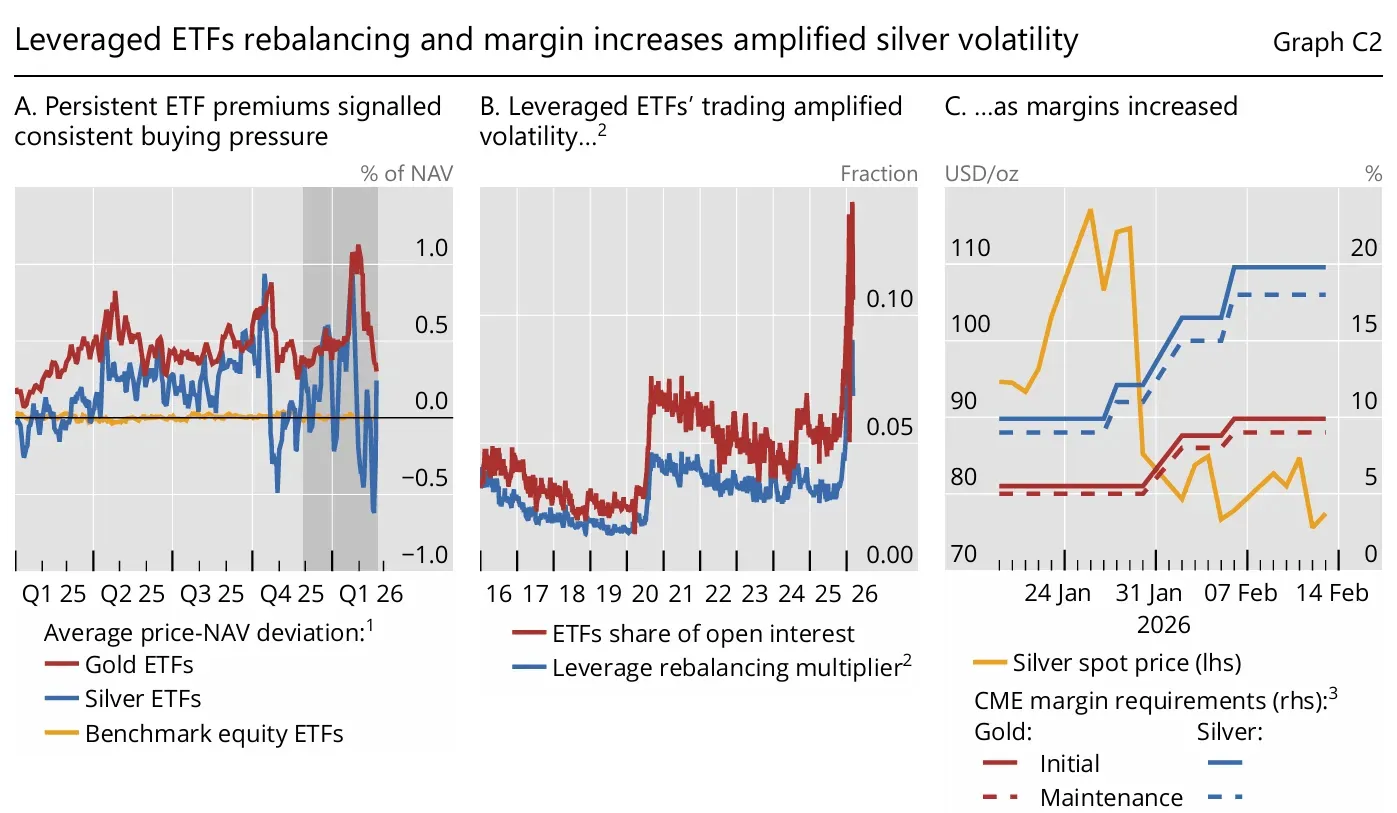

BiS on Silver’s January Collapse

The violent collapse in silver prices at the end of January has prompted renewed scrutiny of how modern financial structures interact with commodity markets. According to analysis released by the Bank for International Settlements, the largest one-day decline in the metal’s history was not solely the product of changing fundamentals or geopolitical repricing. Instead, mechanical trading structures embedded in leveraged exchange-traded funds appear to have intensified the speed and magnitude of the move.

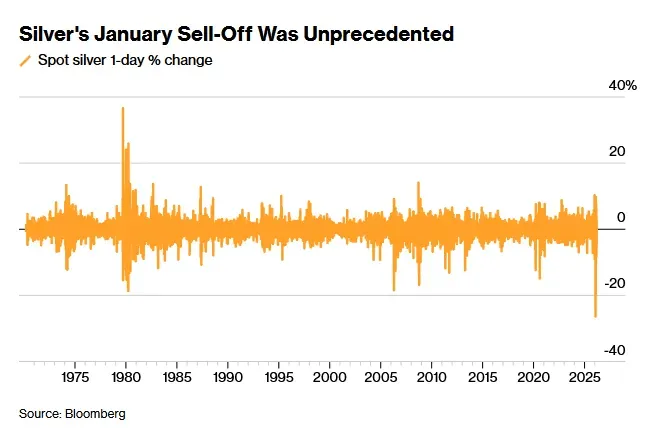

Silver had rallied more than 50 percent in the weeks leading into the event, supported by speculative demand, geopolitical uncertainty, and macro concerns surrounding central bank policy. That advance culminated in a sharp reversal on January 30, when prices fell as much as 36 percent intraday. The BIS argues that the structure of leveraged ETFs created an amplification mechanism that accelerated the decline once prices began to retreat.

The analysis appears in the latest Quarterly Review from the Bank for International Settlements, which examines how retail flows, derivatives markets, and leveraged investment vehicles interact in commodity markets.

Retail Momentum Meets Mechanical Rebalancing

The BIS describes the earlier surge in silver prices as an example of speculative momentum interacting with new access channels for retail investors. Increasingly, investors gain commodity exposure through exchange-traded funds that offer leveraged daily returns.

These products must adjust their exposure at the end of each trading session to maintain their targeted leverage ratio. When prices rise, the funds buy additional futures contracts. When prices fall, they must sell.

“This predictable, momentum-like trading creates feedback loops that reinforce prevailing trends and can distort prices.”

During silver’s sharp reversal, the largest ETF linked to the metal was forced to rapidly reduce its futures exposure as prices declined. Bloomberg estimates suggest more than $3 billion of futures were shed during the rebalancing process.

Because these adjustments occur mechanically rather than discretionarily, the resulting flows can arrive regardless of liquidity conditions in the market.

The Leverage Reset Mechanism

Leveraged ETFs typically target a multiple of daily price movements rather than long-term performance. For example, the ProShares Ultra Silver ETF seeks to deliver roughly twice the daily return of silver futures.

Maintaining that exposure requires daily recalibration.

When markets rise, funds must increase their futures holdings. When markets fall, they must reduce positions to restore the leverage ratio. In trending markets this process can accelerate price momentum.

“The footprint of leveraged ETFs’ destabilizing trading appears to have grown amid the retail-driven exuberance in precious metal markets.”

The BIS notes that the scale of leveraged ETF participation has expanded rapidly as retail trading activity increases and derivatives exposure becomes easier to access through listed funds.

Margin Calls and the Liquidation Spiral

ETF rebalancing was only one part of the dynamic. Futures markets operate on margin requirements, meaning traders must maintain collateral against their positions.

When prices fall sharply, traders holding long futures positions can face margin calls that force them to liquidate contracts.

Those forced sales place additional downward pressure on prices.

“Futures selling combined with leveraged ETF rebalancing created a self-reinforcing loop of lower prices and further margin calls.”

The BIS describes this interaction as a feedback mechanism where price declines trigger liquidation, liquidation drives prices lower, and additional margin calls follow.

Retail Flows and Structural Market Shifts

A broader theme highlighted in the BIS review is the growing influence of retail flows in derivatives-linked commodity markets.

Leveraged ETFs provide simplified access to exposure that historically required direct futures trading. While this expands participation, it also introduces flow dynamics that may be disconnected from physical supply and demand.

Recent data suggest that nearly one-third of ETFs launched in the past year include some form of leverage. Regulators have already expressed concern about increasingly aggressive structures in the ETF market.

“Leveraged products can amplify market dynamics through predictable rebalancing flows that become particularly pronounced during periods of rapid price movement.”

The GoldFix View: Market Structure Matters

For observers of precious-metals markets, the BIS findings reinforce an important distinction between financial positioning and physical supply.

Silver trades within a hybrid structure where futures markets, ETFs, and derivatives flows can dominate short-term price discovery even while underlying industrial and investment demand remains relatively stable. In these environments, price swings may reflect leverage mechanics and margin pressures rather than changes in physical scarcity.

Episodes such as the January collapse illustrate how modern financial plumbing can amplify volatility inside commodity markets that historically were driven primarily by supply, demand, and inventory cycles.

Understanding those structural dynamics is becoming essential for interpreting price action in precious metals and other financialized commodities.