Summary

After one of the sharpest corrections of the current cycle, (and CITI’s recent announcement advising clients to not buy the dip in gold) Crédit Agricole believes the market may be misreading gold’s recent weakness. The bank argues that rising real rates, stronger dollar demand, and central bank selling linked to the Iran conflict have created temporary pressure on prices, but have not altered the structural forces that have supported gold since 2022. Their conclusion is straightforward: buy the dip.

We recommend buying XAU/USD at USD4338, targeting a bounce to USD5420 in the coming quarters, with a stop-loss of USD3800.

Gold’s decline from its January highs has created a familiar narrative across financial markets. Safe haven demand was expected to push prices higher during a period of geopolitical turmoil. Instead, gold sold off. Many investors interpreted that move as evidence that gold had re-coupled with real interest rates and that higher yields would once again dominate the precious metals story.

Crédit Agricole disagrees.

“XAU’s appeal as the ultimate debasement and risk aversion hedge is not necessarily lost.”

The Real Rate Argument

The bank’s first point is that real rates may not be able to rise enough to become a lasting headwind.

Analysts argue that central banks remain trapped between inflation concerns and slowing economic growth. Higher energy prices may lift inflation expectations, but elevated debt burdens across the United States, Europe, Japan, and the United Kingdom limit how aggressive policymakers can realistically become.

In their view, the market may be overestimating the ability of central banks to engineer a sustained rise in real yields.

That matters because the bear case for gold increasingly rests on exactly that assumption.

The 2022 Regime Change

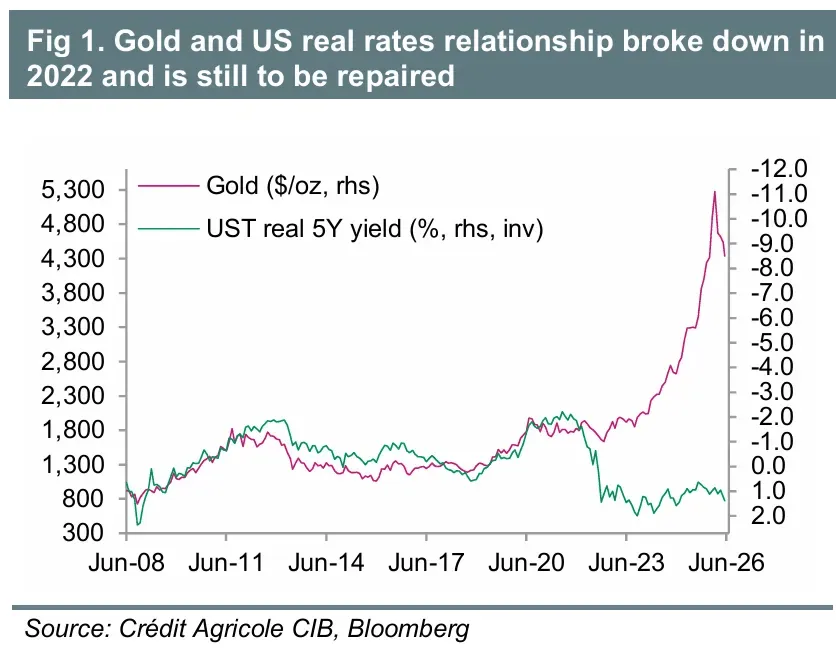

One of the more interesting observations in the report is that the traditional relationship between gold and real rates appears to have weakened dramatically after 2022.

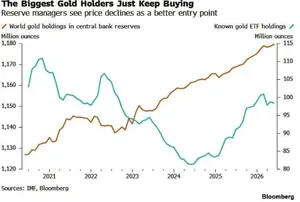

According to Crédit Agricole, the outbreak of the Ukraine conflict accelerated central bank gold accumulation throughout the emerging world, transforming gold from a simple inflation hedge into a broader hedge against currency debasement and dollar concentration risk.

Their chart shows that while real rates have moved significantly over the past several years, gold continued to trend higher anyway.

In other words, the old model may no longer explain the market.

That may ultimately be the most important takeaway from the report. For decades, gold was largely analyzed through the lens of Federal Reserve policy. Higher real rates were viewed as bearish, lower real rates as bullish. Yet the emergence of central banks as the dominant source of demand has altered that framework.

A hedge fund can reduce gold exposure when yields rise. A central bank attempting to diversify reserves operates under a very different mandate. Reserve managers are increasingly focused on neutrality, liquidity, and protection against financial sanctions. Those considerations do not disappear simply because bond yields move higher.

If that shift continues, corrections may increasingly reflect temporary liquidity pressures rather than lasting changes to the underlying demand picture.Collateral Damage From Iran

The bank also believes recent selling pressure may have less to do with gold itself and more to do with secondary effects of the Iran conflict.

Their thesis is that surging oil prices created intense demand for U.S. dollars among energy-importing emerging markets, forcing some central banks to liquidate portions of their gold reserves to secure dollar liquidity. At the same time, weaker energy revenues and growing fiscal pressures may have encouraged some Middle Eastern nations to monetize portions of their gold holdings as well.

If those pressures prove temporary, the selling pressure could fade with them.

That possibility helps explain why Crédit Agricole remains constructive despite the recent weakness. The bank sees the current episode less as a rejection of gold’s role in portfolios and more as a temporary dislocation caused by war-related funding needs, energy market volatility, and short-term reserve management decisions.

Why The Bank Remains Bullish

Crédit Agricole argues that the forces that drove gold higher over the past several years remain largely intact.

The report notes that central bank demand continues to provide structural support while mine supply remains relatively constrained. Analysts also contend that the relationship between gold and real rates is unlikely to fully reassert itself as long as reserve diversification remains a priority for policymakers across the emerging world.

The implication is straightforward. If the drivers behind the recent decline prove temporary while the drivers behind the longer-term bull market remain intact, the correction may ultimately represent an opportunity rather than a warning sign.

“Gold could rebound again once the war in Iran starts to wind down.”

The Bottom Line

Crédit Agricole’s message is simple. Gold’s selloff may have looked like a loss of safe-haven status, but the bank believes it was largely the result of temporary war-related distortions and liquidity pressures rather than a fundamental change in the long-term bull case.

The firm argues that structural support from central bank demand remains intact, real rates face practical limits, and the reserve diversification trend that emerged after 2022 continues to provide a powerful foundation for the market.

Analysts recommend buying gold near current levels around $4,338 per ounce with a target of roughly $5,240 to $5,420 in the coming quarters and a stop-loss at $3,800.

If that assessment proves correct, the recent correction may ultimately be remembered less as the end of the bull market and more as another interruption within it.