When the Fed Loses Control of its Own Domain

Contents

- US Trend Inflation Is 3%

- Core Services Become the Center of the Story

- Deglobalization Changes the Inflation Equation

- Tariffs, Energy, and the Fed

- Analysis: The Fed’s Traditional Inflation Toolkit is Failing

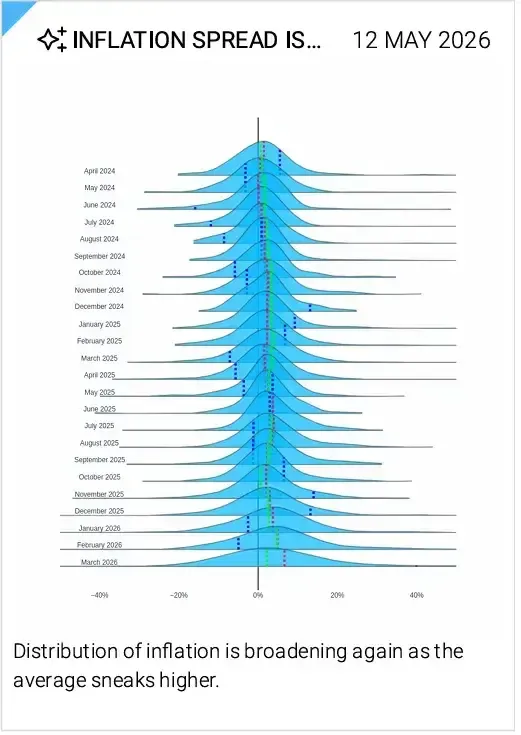

US Trend Inflation Is 3%

Something appears to be changing beneath the surface of U.S. inflation, and TS Lombard argues the shift is becoming structural rather than cyclical.

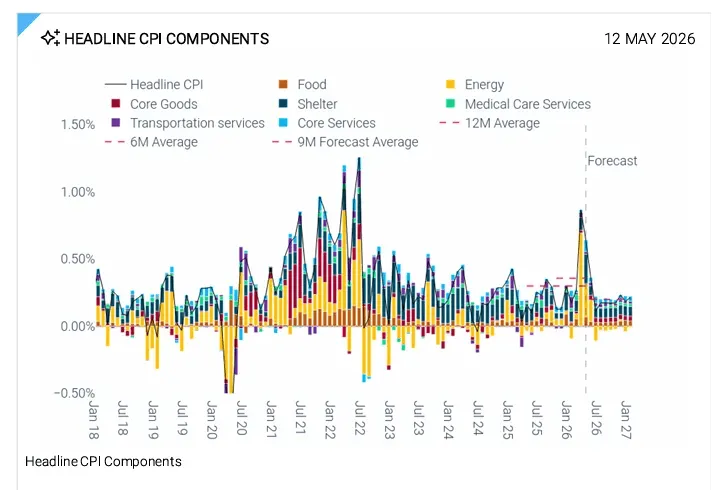

While headline inflation continues to fluctuate with energy and commodity prices, the report contends the more important development is the persistence of core services inflation near 3%, even after one of the most aggressive Federal Reserve tightening cycles in decades. The implication is straightforward: the inflation regime that defined the post-2008 era may no longer apply. Or as we asserted in 2023, it no longer applies at all.

According to TS Lombard analysts Freya Beamish and Alexandros Xenofontos, the combination of deglobalization, tighter labor supply dynamics, tariff pass-through, and geopolitical commodity pressures is creating an environment where inflation settles structurally higher than the 2010s norm. Rather than returning cleanly to the Fed’s 2% target, the report argues the economy increasingly resembles a world where 3% inflation becomes the new equilibrium.

“The labour market give no indication that core services inflation is settling back towards 2%.”

Core Services Become the Center of the Story

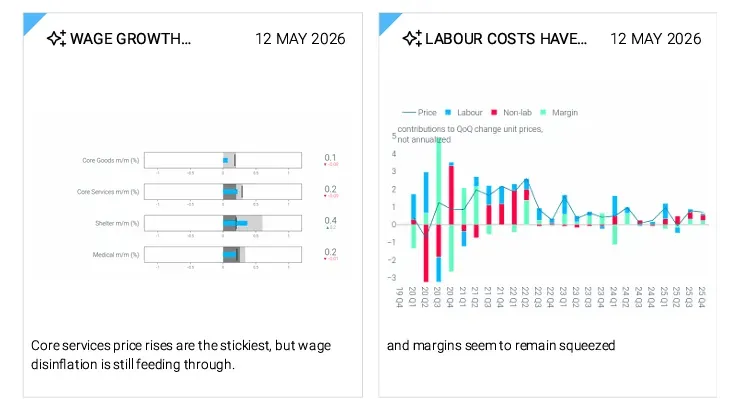

The report places heavy emphasis on core services inflation, particularly services excluding shelter, transportation, medical care, and energy. TS Lombard views this category as the clearest signal of underlying domestic inflation pressure because it is heavily tied to wages and labor market tightness rather than external commodity volatility.

The analysts argue wage growth is no longer decelerating cleanly. Lower immigration flows, demographic constraints, and resilient labor demand are beginning to stabilize wage pressures again after the cooling seen in 2024 and early 2025. Charts throughout the report suggest first-quartile wage growth may already be bottoming while aggregate payroll measures remain firm.

At the same time, firms appear increasingly willing to pass higher labor and input costs through to consumers. TS Lombard argues this reflects a broader shift away from the hyper-globalized economic model that previously suppressed pricing power for decades. In their framework, domestic cost structures matter more today because supply chains are becoming less globally optimized and more politically constrained.

Deglobalization Changes the Inflation Equation

One of the report’s central themes is that deglobalization is widening the relationship between labor costs and CPI inflation. In simpler terms, companies are finding it easier to raise prices relative to underlying wage growth than they could during the globalization era.

Before Covid, cheaper imports, efficient supply chains, and China’s role in global manufacturing acted as major disinflationary forces. TS Lombard argues many of those offsets have weakened. The report specifically notes that declining import penetration outside of AI-related products means domestic costs increasingly dominate pricing behavior.

“Ongoing de-globalisation and shifts in supply chains will leave core goods price inflation higher in the post-Covid cycle than in the 2010s.”

The result is an economy where inflation becomes less sensitive to traditional disinflationary forces. Even areas expected to cool aggressively, including core goods and shelter, are no longer behaving consistently with the old regime.

Tariffs, Energy, and the Fed

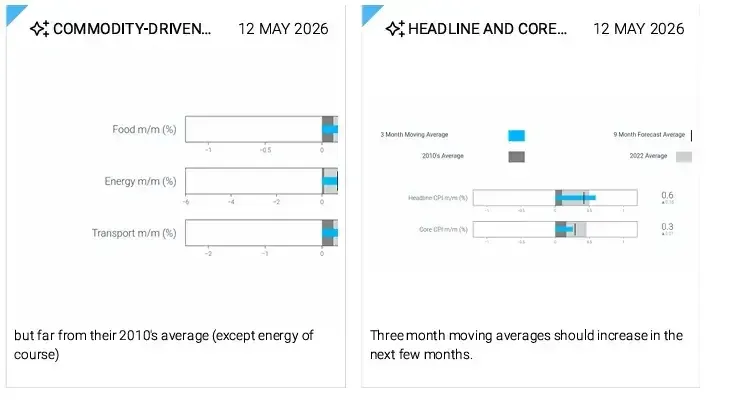

The report also argues tariffs and geopolitical instability are reinforcing inflation pressures rather than creating isolated temporary shocks. TS Lombard points to stronger core goods inflation this year as evidence tariffs are passing through more directly into consumer prices amid resilient demand.

Shipping costs were already rising prior to the latest Middle East tensions, while energy futures still imply elevated oil prices through much of the year. Food inflation may also reaccelerate due to fertilizer disruptions and climate-related pressures tied to El Niño conditions.

TS Lombard ultimately argues the Federal Reserve may face a more difficult policy backdrop than markets currently expect. Several Fed dissents are already moving toward a more hawkish posture as labor market conditions remain resilient with inflation still running around 3%.

The report’s conclusion is not that inflation is spiraling uncontrollably higher. Instead, the argument is subtler and potentially more important: the world that consistently pulled inflation back toward 2% may no longer exist in its prior form.

Analysis: The Fed’s Traditional Inflation Toolkit Stops Working

What makes this TS Lombard report more important is not simply that inflation remains elevated. It is where the inflation remains elevated. The report focuses heavily on services inflation, which historically represents the portion of the inflation curve the Federal Reserve is supposed to control most effectively through monetary policy.

Commodity inflation has always been difficult for central banks to suppress directly. Oil shocks, food shortages, shipping disruptions, and geopolitical supply shocks sit largely outside the Fed’s control. Wage inflation and domestic services inflation, however, traditionally respond more directly to tighter financial conditions because higher rates slow hiring, weaken demand, soften housing activity, and eventually cool labor markets.

That relationship appears increasingly unstable.

TS Lombard’s core argument is that services inflation remains structurally sticky despite years of elevated rates. In practical terms, this means the area of inflation the Fed normally controls best is no longer responding normally to tightening policy. That is a significant development because it suggests monetary policy transmission itself may be weakening under the current economic structure.

We first raised this issue in 2023 within the broader “Anti-Goldilocks” framework. The argument then was that aggressive fiscal spending, industrial policy, infrastructure investment, reshoring initiatives, and labor-intensive manufacturing expansion were offsetting much of the restrictive pressure created by higher interest rates. In effect, one arm of government continued stimulating demand while the other attempted to suppress it.

The result is an economy where labor demand remains structurally firmer than prior cycles, even under elevated rates.

Housing adds another layer to the problem. Higher mortgage rates normally cool shelter inflation more effectively, yet constrained inventory, demographic demand, and lingering structural shortages have reduced the sensitivity of housing costs to tighter monetary conditions. TS Lombard’s discussion of shelter inflation leveling rather than collapsing reinforces this broader issue.

The implication is uncomfortable for markets. If the Fed struggles to suppress domestic wage and services inflation, even after years of tightening, then inflation itself may be considerably more durable than consensus expectations still assume. In that environment, the risk is not simply persistently elevated inflation. The larger risk is that policymakers discover the modern economy has become less responsive to traditional monetary restraint altogether.

That would imply a far rougher inflation cycle than markets currently price.