Boots On the Ground

Two Stories from China today. The first is a news item describing China adding another 5 tonnes of Gold ( the most since early 2025) to its reserves as they bought the dip in March. The second is less obvious but we believe far more important as it pertains to the potential for growing demand in China

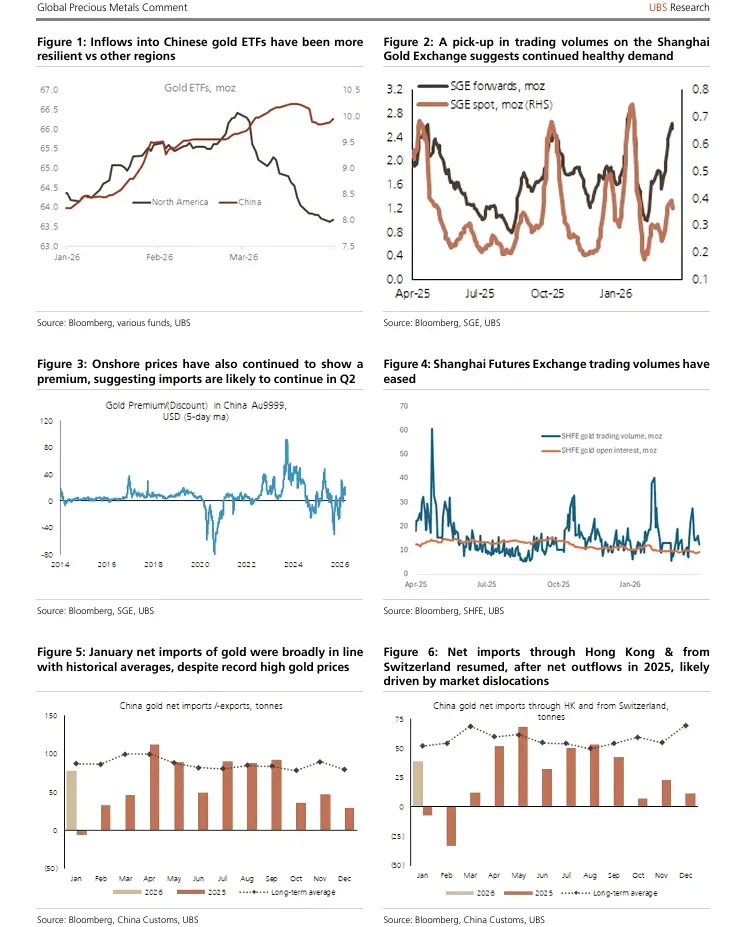

China’s gold demand is shifting from cyclical buying to structural allocation, driven by macro uncertainty, institutional adoption, and supportive policy. Onshore premiums, rising SGE volumes, and resilient ETF inflows confirm sustained strength, while insurance participation and retail platforms broaden demand, reinforcing a durable and increasingly diversified bid beneath the market.

China Holds the Bid

On-the-Ground Signals Point to Persistent Gold Demand

Fieldwork conducted by UBS across China provides a direct read into one of the most important structural drivers in gold today: persistent, policy-supported, and increasingly diversified domestic demand. Conversations with financial institutions, insurers, and market participants confirm that current flows are not episodic. Demand is becoming embedded across multiple channels, supported by macro conditions and regulatory adjustments.

“We introduce a new subcategory… to share what we have learned from our latest trip to China.”

At a high level, Chinese gold demand is transitioning from price-sensitive participation toward structural allocation behavior.

Macro Backdrop

Stagflation Risk and Dollar Skepticism Anchoring Demand

Market participants expressed a consistently cautious macro outlook. The Middle East conflict is viewed as a drag on growth and a source of persistent energy inflation, reinforcing concerns around stagflation.

“The overall sentiment was quite negative… with a lot of the negative impact to the global macro outlook seen to have already been done.”

There is also skepticism toward the durability of the U.S. dollar. The combination of slowing growth, policy uncertainty, and elevated geopolitical risk is shaping allocation decisions at the institutional level.

Within this framework, gold is increasingly viewed as a core portfolio component rather than a tactical hedge.

Institutional Adoption Expanding

Insurance, Banks, and Platforms Drive Incremental Flows

A key structural development is the expansion of institutional participation, particularly among insurance companies. Under a pilot program allowing up to 1% of assets under management to be allocated to gold, roughly half of eligible firms have already begun deploying capital.

“Around half of insurance companies… have started to become more active.”

This introduces a new source of demand that did not exist in prior cycles.

Flows are expected to route through the Shanghai Gold Exchange (SGE), where these institutions are permitted to transact. Early signs of increased SGE turnover suggest that participation is already impacting market activity.

In parallel, banks are scaling gold accumulation products and distributing them through digital platforms. Tax changes have also shifted incentives toward investment gold.

“Retail and institutional investment demand is growing considerably…”

Demand is broadening across both institutional and retail channels.

Market Structure Signals

Price Action vs Conviction

Short-Term Weakness Driving Entry Debate

Despite the constructive backdrop, recent price weakness has introduced near-term uncertainty. The February retracement and continued softness into March have prompted market participants to reassess entry levels.

“A degree of nervousness was palpable… as market participants stress-tested underlying assumptions.”

This has shifted the conversation toward timing rather than direction. Demand has not reversed, but participants are calibrating exposure based on price levels.

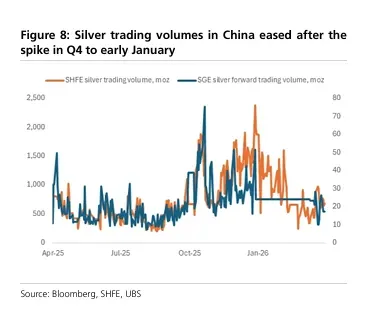

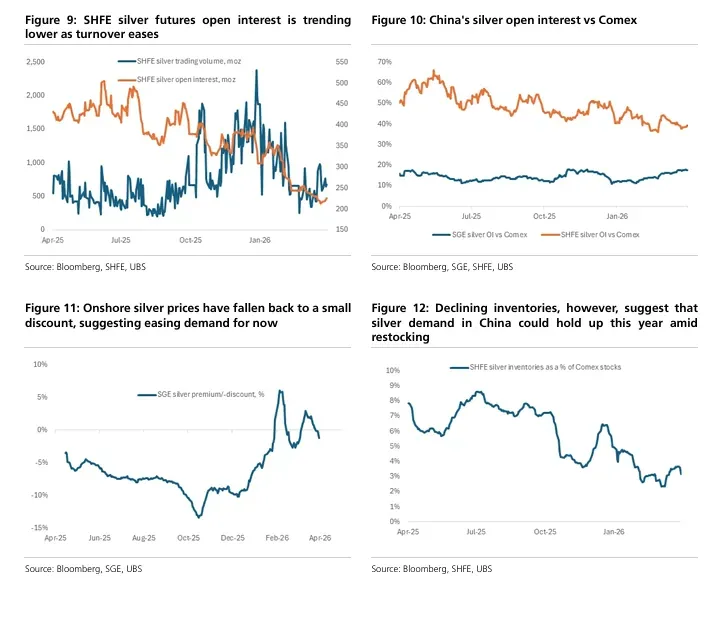

Silver: Strength with Near-Term Moderation

Silver demand has also been strong, supported by both investment interest and structural restocking needs. However, recent data shows some easing in activity following elevated levels earlier in the year.

“Latest data indicates some near-term easing in demand…”

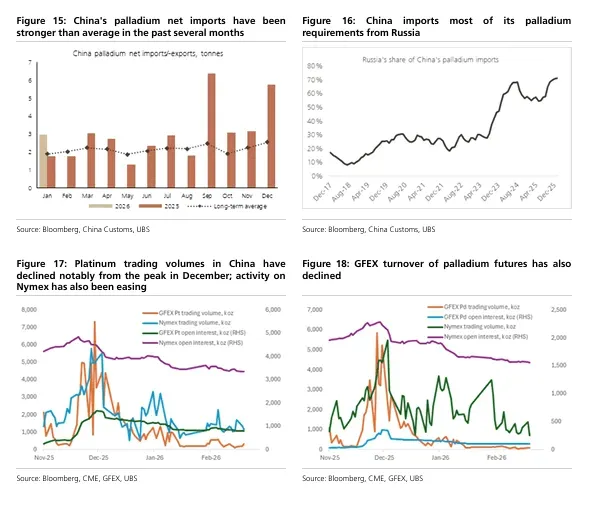

PGMs: Limited Engagement, Diverging Trends

Structural Conclusion

Demand Is Broadening Across Channels

The central takeaway is that Chinese gold demand is evolving in composition rather than peaking.

Institutional participation is expanding through insurance and banking channels. Regulatory frameworks are enabling broader allocation. Macro conditions are reinforcing the role of gold within portfolios. Market indicators continue to confirm active demand through premiums, volumes, and flows.

“Majority… signalled an upside bias to gold price expectations over the medium to long term.”

Short-term uncertainty is influencing timing decisions, but not the underlying direction.

From a structural perspective, this represents a demand base that is becoming more diversified, more institutionalized, and more durable.