Higher in Steps: UBS Sees Copper Marching Toward $15,500

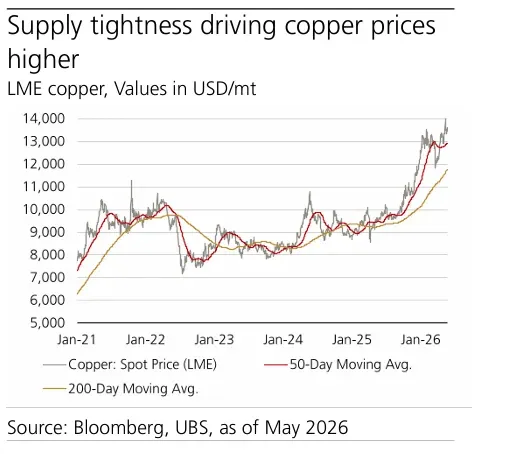

The copper market continues to trade as a supply-constrained industrial system rather than a cyclical commodity market. In a May 22 report titled Higher in Steps, analysts at UBS argue that structural shortages across concentrates, scrap, sulfur, and refined output are forcing prices steadily higher despite mixed global growth signals.

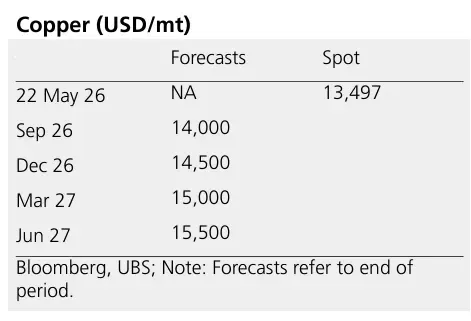

UBS now forecasts copper prices reaching USD 14,000/mt by September 2026, USD 14,500/mt by year-end, USD 15,000/mt by March 2027, and USD 15,500/mt by June 2027. The bank maintains a constructive stance and continues to recommend long exposure to copper, particularly during price pullbacks.

The Market Is Tightening from Multiple Directions

The core thesis behind the report is simple: copper supply growth is struggling to keep pace with electrification-driven demand growth.

According to UBS, sulfur shortages in China have intensified after Beijing imposed new sulfuric acid export restrictions. That has raised costs for higher-cost leaching operations while simultaneously tightening the broader refining chain. At the same time, copper concentrate and scrap availability remain constrained, creating aggressive competition among smelters for feedstock.

Treatment and refining charges (TCRCs), which are often viewed as a gauge of concentrate availability, have effectively collapsed.

“2026 Annual benchmark global treatment and refining charges (TCRCs) [fell] to USD 0/mt… and spot charges below USD -100/mt amid fierce competition among smelters.”

That matters because negative treatment charges imply smelters are effectively paying to secure material. In commodity markets, this is usually a sign of severe upstream tightness.

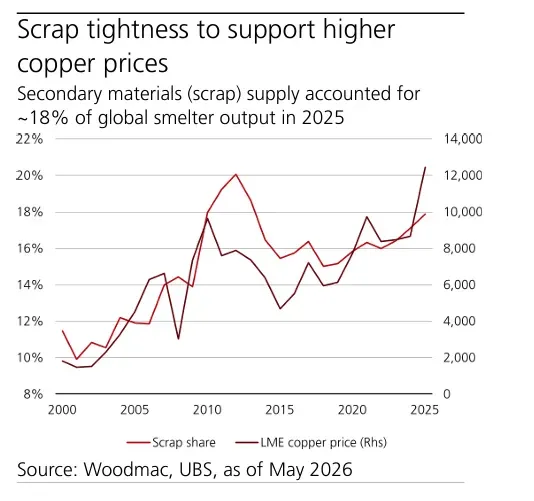

The report also highlights tightening scrap flows. China’s stricter tax compliance standards and invoice quotas are reducing available recycled material, while Japan is increasingly retaining domestic scrap as its own smelters shift toward recycled copper processing.

Electrification Demand Remains Intact

Despite slowing global manufacturing activity, UBS argues the larger structural demand trend remains firmly supportive for copper.

The bank estimates global copper consumption will rise 2.8% in 2026, driven primarily by grid investment, electric vehicle adoption, renewable infrastructure, and the continued expansion of data centers.

This is an important distinction. Traditional cyclical demand indicators, such as manufacturing PMIs, have softened around the margins, yet copper demand tied to electrification infrastructure continues to expand.

China remains central to that story.

While January-April copper imports into China declined year-over-year, April imports alone still rose 2.3% compared to the same month last year, suggesting underlying physical demand remains resilient despite broader economic uncertainty.

UBS describes current demand signals as “mixed,” though the broader directional trend remains constructive because the energy transition continues requiring massive copper intensity across grids, transportation systems, and industrial infrastructure.

Chile and Peru Continue to Disappoint

On the supply side, the market’s largest producing regions continue struggling to expand output.

UBS notes that disruptions in Chile and Peru remain a major constraint on global supply growth. Chilean production alone has fallen 6% year-over-year so far this year.

Meanwhile, Freeport’s Grasberg mine is now not expected to fully resume operations until early 2028, adding another delay to anticipated supply normalization.

As a result, UBS expects refined copper supply growth to rise just 1.7% in 2026, well below the pace needed to close the widening supply gap.

The bank now projects the global copper market deficit will widen to 520,000 metric tons in 2026, more than double the estimated 203,000 metric ton deficit recorded in 2025.

That widening imbalance remains the foundation of UBS’s bullish view.

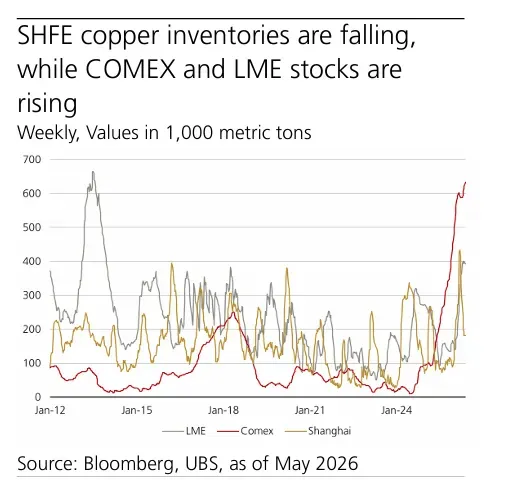

Inventory Flows Reveal a Market Repositioning

One of the more interesting sections of the report involves inventory movements across global exchanges.

Shanghai Futures Exchange (SHFE) inventories have fallen sharply since March, declining by 178,500 metric tons. Meanwhile, inventories at COMEX and the LME have risen.

UBS believes much of the increase in COMEX inventories reflects positioning ahead of potential US copper tariffs.

Market participants are now awaiting further updates from the US Department of Commerce after proposals emerged for phased tariffs on imported refined copper, beginning at 15% in 2027 and potentially rising to 30% by 2028.

In practical terms, the copper market increasingly appears to be fragmenting geographically, with inventory behavior being influenced as much by industrial policy and trade strategy as by traditional cyclical demand.

UBS Remains Constructive

UBS concludes that the market still has room for additional speculative participation. Net-long LME positioning has risen moderately, though the bank argues positioning remains far from extreme levels.

The report ultimately frames copper as a market facing a classic structural squeeze: demand tied to electrification continues expanding while permitting delays, declining ore grades, scrap shortages, and geopolitical fragmentation continue constraining supply growth.

“Given the anticipated market deficit, we expect any price weakness to be shallow and short-lived.”

In that environment, UBS views pullbacks toward USD 12,800-13,000/mt as buying opportunities rather than trend reversals.