JPMorgan Says the Long-Term Bull Market Is Intact, Even If the Fed Controls the Next Move

Gold investors have spent much of the past four years watching central banks rewrite the rules of the market. Massive official-sector buying helped break gold’s traditional relationship with real interest rates and supported prices even as bond yields climbed.

JPMorgan believes that regime has temporarily changed. In its latest precious metals outlook, the bank argues that slowing physical demand and a pause in aggressive central bank accumulation have allowed ETF flows to once again become the market’s marginal price setter, reconnecting gold with real yields and Federal Reserve expectations.

“Amid a drop in buying intensity from other demand sectors for now, rate-sensitive ETF flows have regained marginal pricing power in gold.”

That distinction matters.

JPM is not arguing that the structural case for gold has weakened. Rather, it believes the market has entered an interim phase where macroeconomic data and interest-rate expectations have become more influential because other sources of demand have temporarily stepped back.

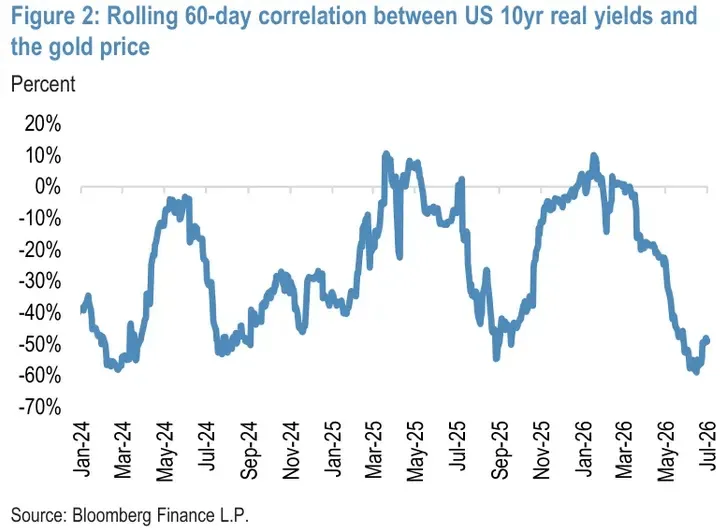

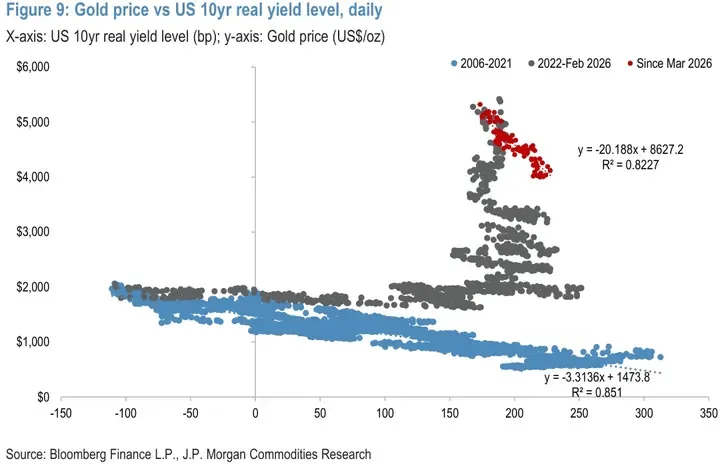

JPMorgan shows gold re-establishing its historical inverse relationship with real yields as ETF flows regain influence over short-term pricing.

The report traces this shift back to the post-2022 period.

When central banks dramatically accelerated gold purchases following the freezing of Russian reserves, official buying became large enough to offset persistent ETF selling. Gold continued climbing despite rising real yields because sovereign demand overwhelmed traditional Western investment flows.

According to JPM, today’s environment looks different.

Chinese retail demand has softened, Indian imports remain constrained by policy, and central banks continue buying but with less intensity than during the peak accumulation phase. The result is that ETF flows once again exert greater influence over marginal pricing.

“ETF flows now back in the driver’s seat for gold prices.”

The report illustrates how official-sector buying offset ETF outflows after 2022 before market leadership gradually shifted back toward rate-sensitive investors.

That helps explain JPM’s revised outlook.

Rather than expecting an immediate return to record highs, the bank forecasts gold averaging $4,300/oz in the third quarter and $4,500/oz in the fourth quarter of 2026, reflecting a more range-bound market while investors wait for greater clarity from the Federal Reserve.

Importantly, those forecasts are not based on a bearish long-term view.

JPM continues to argue that the forces underpinning official-sector diversification and physical accumulation remain in place.

“We still retain a long-term bullish outlook for gold… the debasement theme is not dead, just currently significantly overshadowed.”

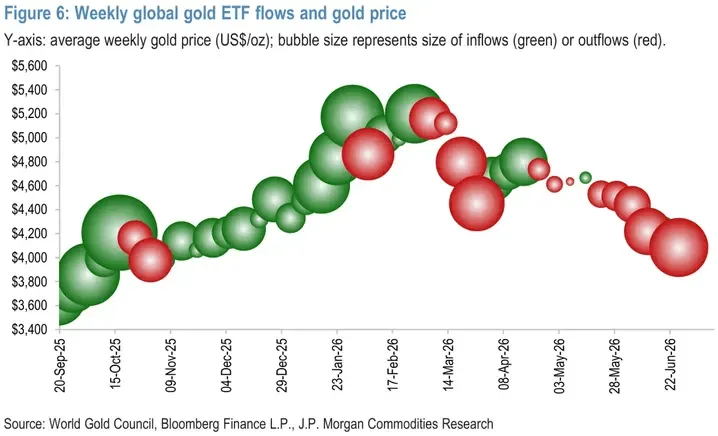

ETF outflows have become increasingly important in determining short-term price direction as other demand sources temporarily pause

The report also highlights the risks.

Should inflation remain firm or labor-market data surprise to the upside, markets could price earlier Federal Reserve tightening. Under that scenario, JPM warns gold could briefly test levels below $4,000 before longer-term buyers return.

Yet even in its downside scenario, the report never abandons the broader bull thesis.

Instead, it argues investors should distinguish between tactical headwinds created by monetary policy and the structural drivers that have reshaped the gold market since 2022.

That distinction may be the report’s most important message.

Gold’s long-term foundation has not materially changed.

Its short-term driver has.

Gold has become increasingly sensitive to movements in real yields as the Federal Reserve once again dominates short-term market psychology.

GoldFix Comment

JPM’s report is valuable because it separates market structure from market direction.

The structural story remains remarkably consistent with what we’ve been discussing for years: central banks continue diversifying reserves, physical demand remains a long-term pillar, and gold still serves as monetary insurance in a world of elevated sovereign debt and geopolitical fragmentation.

The tactical story, however, has shifted.

When one group of buyers temporarily steps back, another naturally becomes the marginal price setter. Today that group is ETF investors responding to real yields and Fed expectations.

Markets often confuse a change in who sets the price with a change in why the asset is owned.

JPM argues they are not the same thing.

If history is any guide, leadership within the gold market can rotate several times during a secular bull cycle. The cleaner read is that today’s Fed-driven consolidation may ultimately prove to be another chapter within a much larger structural trend rather than its conclusion.

About the Author

Vincent Lanci is a commodity trader, Professor of MBA Finance (adj.) , and publisher of theGoldFixnewsletter.