China, Copper, and the Metal Leaving the Rest of the World Short

On June 1, 2026, Goldman Sachs raised its copper price forecasts, arguing that the market has become materially tighter than expected. The change was driven by two developments: slower mine supply recovery and stronger-than-anticipated U.S. imports. Together, those forces are creating a shortage everywhere outside the United States, which is the market that ultimately determines the London Metal Exchange (LME) copper price.

In practical terms, Goldman is making a simple argument. The world is producing less copper than expected, while the United States continues pulling more copper into domestic inventories. The result is a tightening ex-U.S. market and a higher equilibrium price.

Supply Recovery (Scrap) Has Fallen Behind Expectations

The first pillar of the bullish thesis is supply.

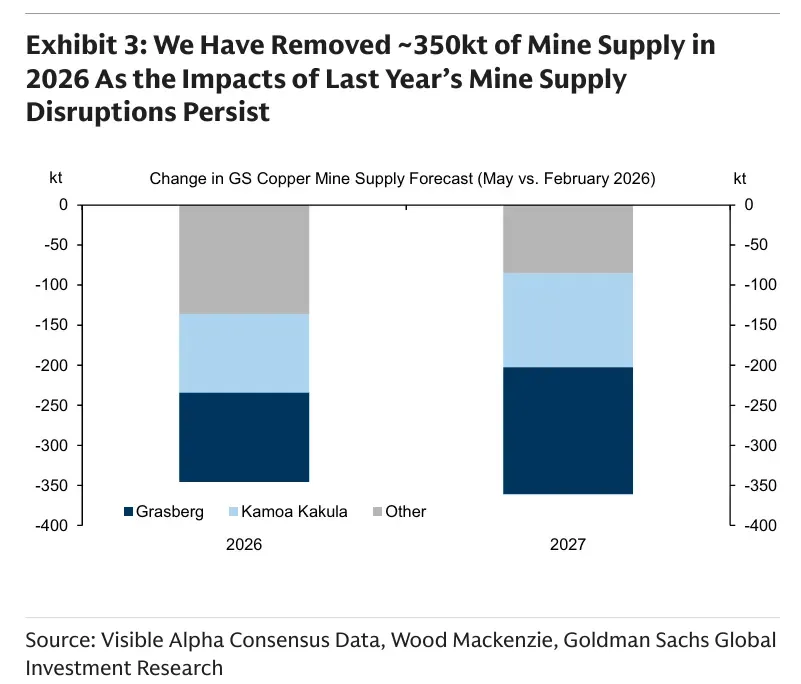

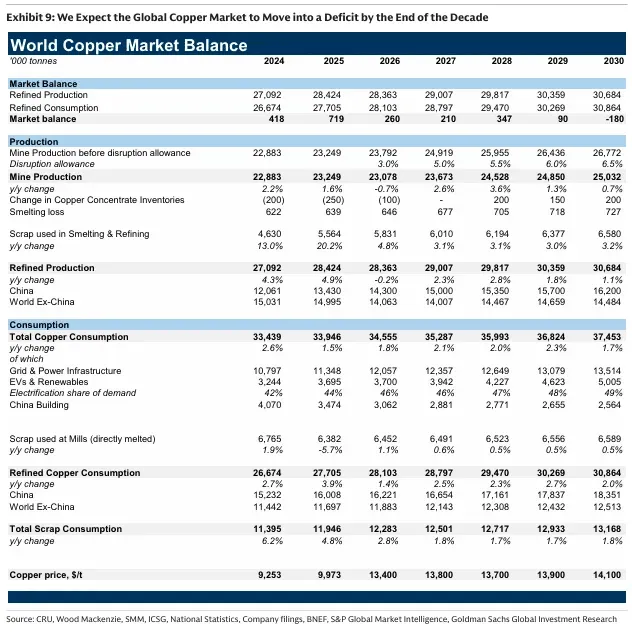

Goldman reduced its 2026 global mine supply forecast by approximately 350,000 tonnes after reassessing production recoveries at two critical operations: Grasberg in Indonesia and Kamoa-Kakula in the Democratic Republic of Congo. The bank no longer expects either mine to return to full capacity until 2028.

That revision matters because copper has spent the past several years relying on a relatively small number of large projects to meet growing demand. When major mines underperform, there are few immediate replacements available.

The report estimates that supply disruptions alone account for roughly half of the tightening seen in Goldman’s revised balance projections.

At the same time, scrap copper is providing less relief than expected.

Chinese domestic scrap output is down roughly 12% year-over-year, partly because tighter invoice compliance requirements have made sourcing scrap more difficult through official channels. As a result, imported scrap remains in high demand and scrap availability has not been sufficient to offset tightening refined copper markets.

“China’s domestic scrap output is down 12% YoY YTD.”

The implication is straightforward: supply growth remains constrained even as prices hover near record levels.

The Copper Is Going to America

The second pillar of the thesis is arguably more important.

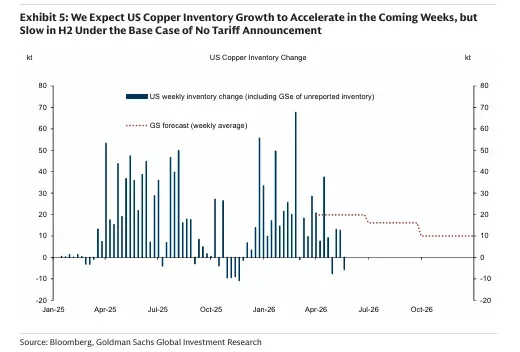

While mine disruptions tighten the global market, Goldman argues that U.S. imports are tightening the market where prices are actually set.

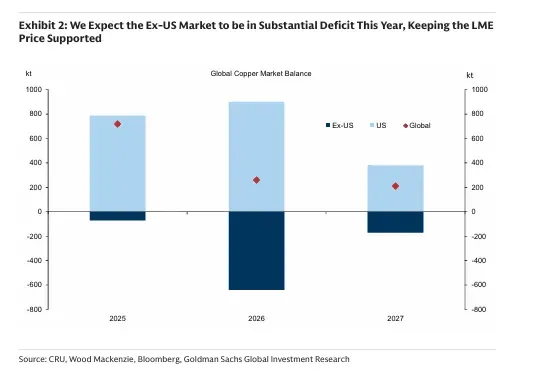

The bank notes that U.S. imports exceeded expectations during the first half of 2026. As a result, it increased its forecast for U.S. copper inventory accumulation to 900,000 tonnes from 550,000 tonnes previously.

This creates a somewhat unusual dynamic.

Copper moving into the United States is effectively removed from the inventory pool available to the rest of the world. Even if global supply remains unchanged, metal accumulating inside U.S. warehouses leaves less available for consumers elsewhere.

Goldman now expects the ex-U.S. copper market to post deficits of 640,000 tonnes in 2026 and 170,000 tonnes in 2027, substantially larger than prior forecasts.

This distinction between the global balance and the ex-U.S. balance is central to the report. The bank argues that LME prices respond primarily to conditions outside the United States because that is where international pricing occurs.

Strategic Demand Is Changing Copper

The report also highlights a structural shift occurring on the demand side.

Historically, copper demand was heavily tied to housing, construction, and industrial activity. Increasingly, however, demand growth is coming from strategic sectors.

Goldman expects more than 60% of copper demand growth through 2030 to originate from grid expansion and power infrastructure investments. Artificial intelligence, data centers, defense spending, and energy security initiatives are becoming major drivers of copper consumption.

The bank argues that these sectors are less sensitive to economic slowdowns and less sensitive to high prices than traditional industrial demand.

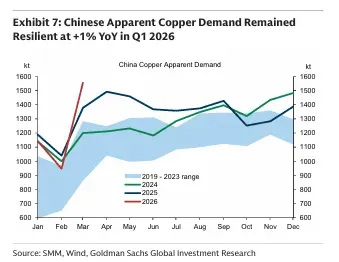

Chinese copper demand provides a recent example. Despite copper trading near record highs, Chinese apparent demand remained positive during the first quarter of 2026, supported by power grid investment even as other sectors softened.

“We expect more than 60% of copper demand growth by 2030 to come from grid and power infrastructure.”

This increasingly strategic nature of demand helps explain why copper prices have remained elevated despite slowing global growth concerns.

Higher Targets, But Limited Near-Term Upside

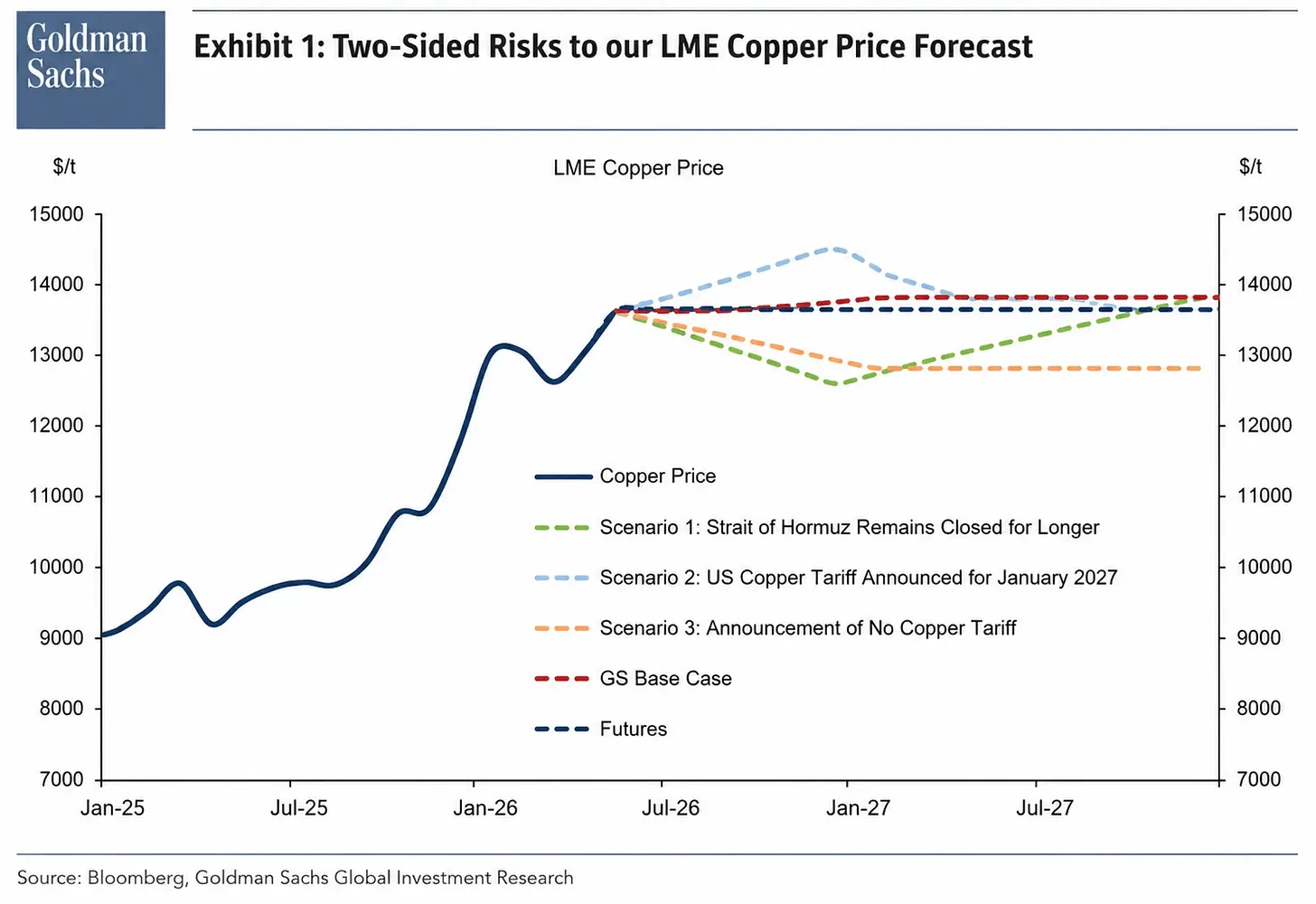

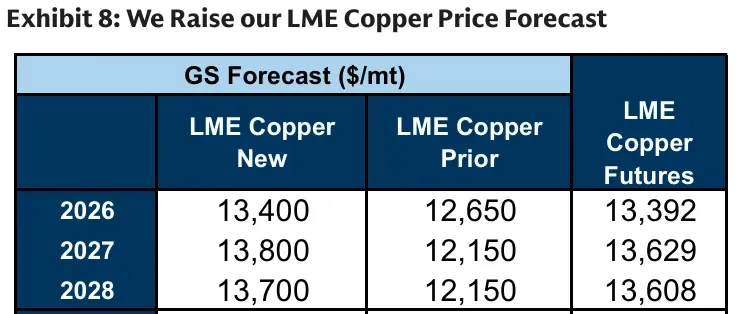

Goldman raised its end-2026 copper target to $13,735 per tonne and its average 2027 forecast to $13,800 per tonne, up sharply from prior estimates.

Yet the report is not calling for an immediate explosive rally.

Copper already trades near those levels, meaning Goldman’s base case is largely one of persistence rather than acceleration. Prices remain supported because inventories outside the United States are tightening, mine supply remains constrained, and strategic demand continues to expand.

If the United States announces a future copper tariff beginning in January 2027, Goldman expects imports to accelerate even further as buyers rush to secure material ahead of implementation. Under that scenario, copper prices could move above $14,000 per tonne during the second half of 2026.

The Bigger Picture

The report ultimately describes a market that is becoming increasingly strategic.

Supply growth is struggling to keep pace with demand. Copper inventories are being redirected into the United States. Grid infrastructure, AI expansion, defense spending, and energy security initiatives continue to absorb growing amounts of metal.

For years, the copper story centered on electrification. Goldman now suggests the next phase may be broader than that. Copper is increasingly becoming a metal tied to national infrastructure, industrial policy, and strategic stockpiling.

In that environment, prices may no longer be determined solely by traditional economic cycles. They may increasingly reflect competition for physical supply in a world where governments and industries view copper as a strategic asset rather than simply another industrial commodity.