Recall, the Ukraine war started and Gold caught a nice bid in February of 2022 only to run into Fed tightening in April that obliterated paper bids for 5 months. Right now the market is predicting that the Fed will tighten just as they did in 2022. That’s why Gold is giving back gains.”

Correction, Consolidation, or Something Different?

Should gold investors be disappointed that the metal has failed to extend beyond its January record high above $5,500 per ounce? Or should they take comfort in the fact that, despite a meaningful retracement, the decline has so far been relatively contained by historical standards?

The question is worth asking because gold’s price history over the past two decades suggests that major advances are typically followed by substantial corrections, even when the broader secular uptrend remains intact. The rally from September 2022 through January 2026 was extraordinary by any measure, with gold appreciating 245% before peaking at $5,594.82 per ounce on January 29.

History suggests that gains of that magnitude are rarely digested without a period of significant consolidation.

The previous major bull market began from the October 2008 low of $697.45 per ounce and culminated in September 2011 at what was then a record high of $1,884.40. Gold gained approximately 170% during that advance. The subsequent correction proved lengthy and painful, with prices declining 37% to a low of $1,191.35 by August 2018.

The next major cycle saw gold rise from that 2018 low to $2,072.49 by August 2020, representing a 74% gain. That move was followed by a 22% decline that ultimately bottomed at $1,620.20 in September 2022.

Taken together, those cycles reveal two important characteristics of gold’s long-term behavior. First, larger rallies have historically been followed by larger corrections. Second, the rallies themselves tend to occur over much shorter periods than the subsequent consolidation phases.

Against that backdrop, gold’s decline since January appears relatively modest.

After reaching an all-time high of $5,594.82 on January 29, gold fell roughly 24% to close at $4,328.92 on Friday. Given the scale of the preceding advance, some market participants may argue that a deeper retracement remains possible over the coming months or even years before the next leg higher develops.

That conclusion, however, assumes the forces driving previous gold cycles remain largely unchanged.

There is always danger in declaring that “this time is different.” Financial history is filled with examples of investors making precisely that argument shortly before being proven wrong. Yet the most recent gold rally differed from prior cycles in one important respect: several powerful demand drivers were all operating in the same direction simultaneously.

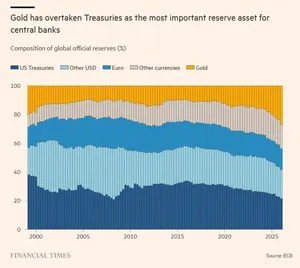

The first was sustained central bank accumulation. The second was strong physical demand from the world’s two largest consumer markets, China and India. The third was a broad-based investor preference for gold as a hedge against uncertainty, often referred to as the “fear trade.”

That fear manifested in several forms. Investors worried about persistent inflation. They worried about worsening geopolitical tensions. Following Donald Trump’s return to the White House, many also expressed concerns that U.S. policy could weaken confidence in the dollar’s role as the world’s reserve currency and, by extension, challenge the foundations of American financial dominance.

Those concerns helped fuel one of the strongest advances in modern gold market history.

More recently, however, several of those supporting factors have begun to moderate.

Central Bank and Consumer Buying Ease

According to the World Gold Council, central banks purchased 243.7 metric tons of gold during the first quarter of 2026, a 3% increase from the same quarter a year earlier.

While still historically robust, the pace of official-sector buying has flattened. Since the beginning of 2025, quarterly purchases have generally stabilized around the 200-ton level. That remains below the exceptionally strong period between mid-2022 and the end of 2024, when central bank purchases exceeded 300 tons per quarter in five separate quarters and fell below 200 tons only once.

Consumer demand has also softened.

Chinese jewelry demand totaled 85.2 tons during the first quarter, down 31% from the same period in 2025. Indian jewelry demand fell 19% to 66.1 tons.

On a global basis, jewelry demand declined 25% year-over-year to 260.2 tons.

The primary reason appears straightforward: higher prices are beginning to ration demand.

In India, policymakers have gone a step further. The government has increased taxes on gold imports in an effort to curb purchases and reduce pressure on the country’s balance of payments.

Investment demand has weakened as well.

Gold-backed exchange-traded funds recorded inflows of 62 tons during the first quarter, a 73% decline from the corresponding quarter in 2025.

As a result, total global gold demand fell 9% year-over-year to 1,195.9 tons in the first quarter of 2026, down from 1,315.6 tons during the same period last year.

Viewed through that lens, gold’s roughly 20% correction since January may actually represent a relatively resilient performance.

Several of gold’s traditional demand pillars have softened, yet prices remain well above historical trend levels.

The Market Has Cycled Back Toward Monetary Policy

The more important development may be that gold is currently trading less on traditional physical demand metrics and more on expectations surrounding monetary policy again.

Recent price action relative to crude oil offers a useful example.

During periods when oil prices rise because of tensions surrounding the ongoing conflict involving the United States and Iran, gold has often struggled. Conversely, when oil prices retreat on hopes of a diplomatic resolution, gold has tended to recover.

At first glance, that relationship may appear counterintuitive.

The connection lies in interest-rate expectations.

Higher oil prices increase inflation risks, making central banks less likely to ease policy and reducing expectations for interest-rate cuts. Lower oil prices have the opposite effect, encouraging markets to price in a more accommodative policy path.

For gold, which generates no yield, those expectations matter enormously. Whether the Fed policy will be a headwind ( as in inflationary war fears) or a tail wind ( as in war aftermath) frequently makes all the difference. Just as it did when the Ukraine war started.

The Ukraine War Forced Fed Tightening

Recall that gold initially responded exactly as one would expect following the outbreak of the Ukraine conflict in February 2022, rallying sharply as investors sought safety amid rising geopolitical uncertainty.

That advance, however, collided with the Federal Reserve’s aggressive tightening campaign beginning in April, which pressured paper-market demand and drove a significant correction that lasted roughly five months. Yet while speculative and financial flows retreated, physical buyers continued accumulating metal throughout the decline.

Today, a similar dynamic appears to be developing. Markets are increasingly pricing in the possibility that the Federal Reserve will maintain a tighter policy stance than previously expected, much as it did in 2022. Gold’s recent pullback reflects that shift in expectations rather than a deterioration in the underlying physical demand picture.

Lower interest rates generally improve the relative attractiveness of non-yielding assets. Higher rates do the opposite.

As a result, gold’s short-term direction increasingly appears tied not to jewelry demand, central bank purchases, or ETF flows, but to shifting expectations around inflation, interest rates, and the geopolitical developments influencing both.

In that sense, gold has become increasingly sensitive to developments surrounding the Iran conflict and its implications for energy markets. Like many other financial assets, the metal is currently trading as much on macroeconomic expectations as on its traditional supply-and-demand fundamentals.

The result is a market that remains historically strong, yet one whose next major move may depend less on how much gold is being bought and more on how investors interpret the path of inflation, interest rates, and global geopolitical risk.

Bottom Line

Gold has returned to its traditional role as a barometer of monetary policy again, and at the moment it appears to be signaling concern that the Federal Reserve may remain more hawkish than markets had anticipated.

The underlying fundamentals that drove gold’s advance have not changed. What has changed is awareness. When GoldFix was launched, the objective was to highlight a shift in the monetary and reserve landscape that few market participants were discussing. Today, those same themes are increasingly understood and widely recognized. Gold’s importance as a monetary asset is no longer a niche conversation. It has reentered the mainstream investment narrative.

Now ask yourself: What happens if the Fed doesn’t tighten as it failed to do in 1976 in an economically similar situation? Bond yields will rise but this time they will take Gold with them as it becomes apparent the Fed is not serious about inflation

Source for data: Reuters