Under scenarios involving renewed macro hedge accumulation and accelerated diversification away from Western assets, gold prices could reach between $5,700 and $6,100.

Goldman Sachs argues gold’s recent sell-off reflects positioning unwinds and higher-rate repricing, not structural weakness. Supply-driven inflation pressures gold short term, but normalized positioning, expected Fed easing, and strong central bank demand support a medium-term rebound, with upside driven by portfolio reallocation and downside limited to liquidation scenarios.

Plus, we note a callback to their first report telling clients to Sell Bonds and Buy Gold.

Constructive Gold Amid the Iran Sell-Off

In the latest report from Goldman Sachs, analysts Lina Thomas and Daan Struyven argue that the recent 15% decline in gold prices to approximately $4,580 is best understood as a function of positioning and macro repricing rather than a breakdown in gold’s structural role within portfolios.

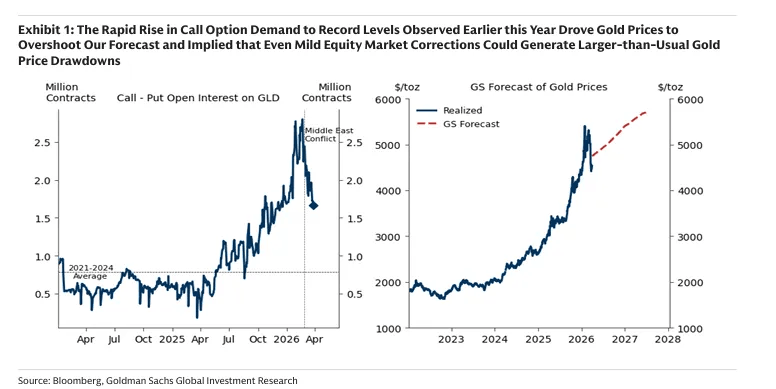

“The rapid rise in call option demand… implied that even mild equity market corrections… could generate larger-than-usual drawdowns in gold prices.”

The report identifies the initial condition for the sell-off as an overshoot driven by record call option demand earlier in the year. This buildup in convex positioning left gold exposed to liquidation once equity markets corrected. Margin-related selling, rather than a shift in fundamental demand, became the dominant driver, with prices moving through the bank’s previously identified lower bound near $4,700/toz.

Alongside positioning, the macro environment shifted materially. The conflict is characterized as an energy supply disruption with upside risks to inflation, prompting markets to reprice the Federal Reserve path toward no rate cuts. Under this repricing, Goldman Sachs estimates fair value for gold near $4,550/toz, placing current levels within a macro-consistent range.

“Under such a hypothetical flat Fed rate path, our estimate of today’s fair value would be around $4,550/toz.”

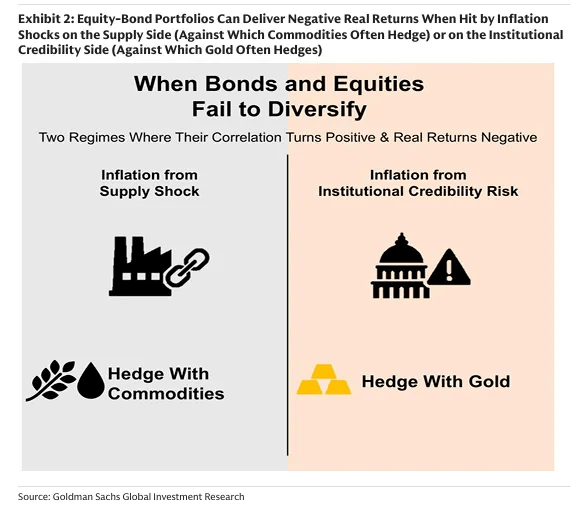

Two Regimes of Inflation and Gold’s Role

A central framework within the report is the distinction between two forms of stagflation, which determine gold’s performance profile.

“Gold on its own is not a sufficient stagflation hedge… there are two distinct stagflationary regimes… and gold behaves differently across them.”

The first regime is defined by institutional credibility risk, where markets question central bank control over inflation. In this environment, historically associated with the 1970s, gold performs strongly as a store of value outside the financial system.

The second regime is supply-driven inflation, where disruptions raise prices while weakening growth. In these conditions, gold typically underperforms in the initial phase. Higher yields increase the opportunity cost of holding gold, and equity market stress drives margin-related liquidation. The current environment is explicitly categorized within this second regime, explaining the recent price behavior.

Central Bank Flows and Reserve Dynamics

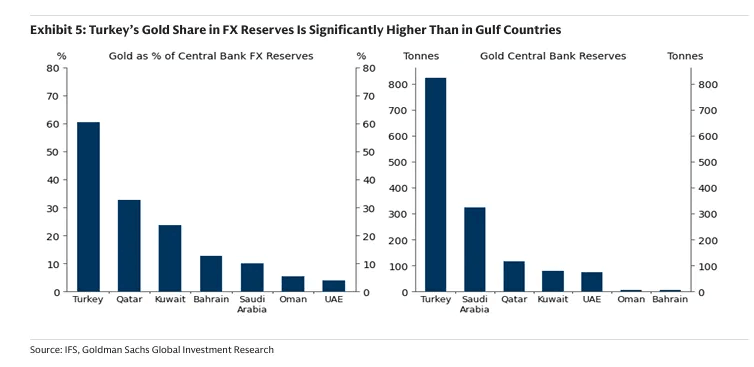

The report addresses concerns that central bank selling contributed to the decline, focusing on Turkey’s reported gold sales and swaps of approximately 52 tonnes.

“These central bank gold sales have not been a dominant direct driver of the selloff.”

Indeed. Given the magnitude and seeming urgency of the liquidation, Gold should have been much much lower based on history. Who was buying taht gold is an important question to ask.

The analysis concludes that the scale of these flows is insufficient to explain the magnitude of the move. Furthermore, the report expresses skepticism that Gulf economies will follow a similar path. Given their reserve structures and dollar-peg regimes, these countries are more likely to manage currency pressures through U.S. Treasury liquidation rather than gold sales.

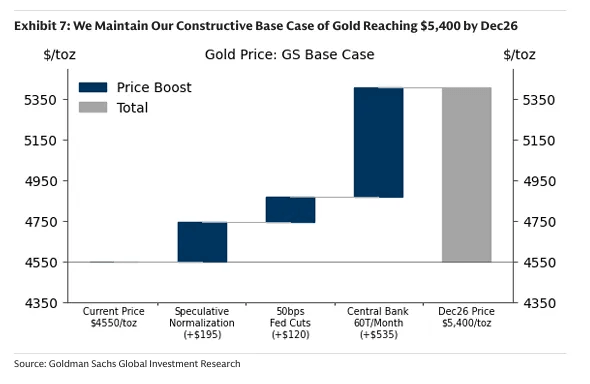

Reconstructing the Path to $5,400

Goldman Sachs maintains its base case of $5,400/toz by end-2026, supported by three primary drivers.

First, speculative positioning has reset. Net positioning on COMEX has declined to the 39th percentile, and the call option overhang has largely been unwound. A normalization of positioning alone is estimated to add approximately $195/toz to prices.

Second, the report incorporates an expected easing cycle. The bank’s economists project 50 basis points of Federal Reserve cuts in 2026, contributing an estimated $120/toz.

Third, central bank demand remains a structural support. The base case assumes purchases averaging 60 tonnes per month, above the recent trend, contributing approximately $535/toz.

“Central bank demand remains a key medium term support… allowing central bank buying to re-accelerate.”

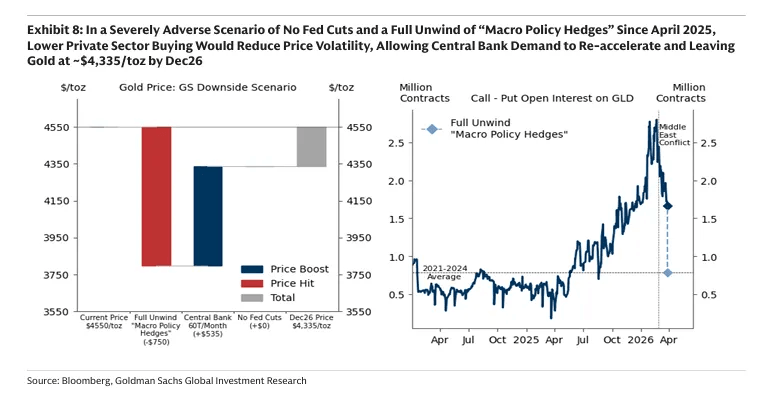

Defining the Downside Scenario

While positioning has largely normalized, the report outlines a defined downside risk tied to prolonged disruption in the Strait of Hormuz and further equity market deterioration.

In such a scenario, investors could unwind remaining macro policy hedges, pushing gold toward approximately $3,800/toz.

“Gold could overshoot to the downside, potentially falling as low as $3,800/toz.”

This outcome is presented as unlikely, but it establishes a lower bound for liquidation-driven price action under adverse conditions.

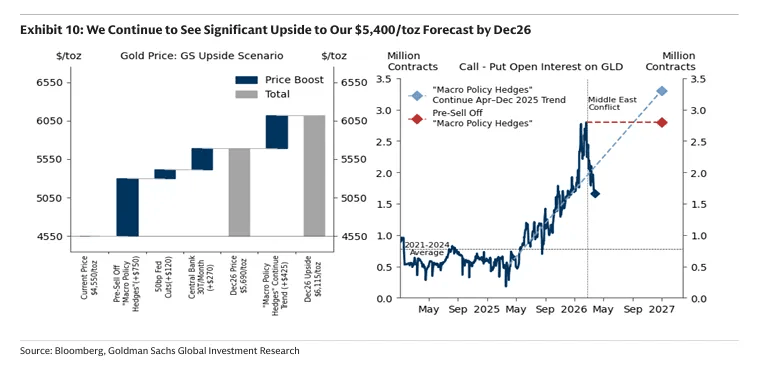

Upside Convexity and Allocation Sensitivity

Despite near-term downside risks, the report emphasizes that upside potential remains significant, particularly through private sector allocation dynamics.

“Each 1bp increase in US private sector portfolio allocation to gold raises prices by roughly 1.5%.”

Current allocations remain low, with ETF holdings representing approximately 0.2% of U.S. private sector portfolios. This creates a convex upside profile, where small reallocations can generate disproportionate price effects.

Under scenarios involving renewed macro hedge accumulation and accelerated diversification away from Western assets, gold prices could reach between $5,700 and $6,100.

Conclusion

The report frames the recent decline as a transition from an overextended, option-driven market to a cleaner structure defined by reduced speculative excess and normalized positioning. The forward path is shaped by central bank demand, policy evolution, and portfolio allocation dynamics, with medium-term risks skewed toward higher prices once macro conditions stabilize.